Changing Quadrants – by Westminster Asset Management

With many asset markets moving higher, Westminster Asset Management Investment Strategist Peter Lucas highlights some early and potentially key changes to his economic models. Peter discusses the impact of inflation and economic growth on markets and believes that signs of rising inflation could have profound implications for markets going forward.

Most investors think about markets in terms of asset classes. Equities versus bonds. Growth versus value. US versus Europe. Risk-on versus risk-off. But most major market moves can ultimately be explained by changes in just two variables: economic growth and inflation, which together create four broad macroeconomic environments – or “quadrants” – with each favouring a different set of assets.

For much of the period following the Global Financial Crisis, investors operated in a world of weak inflation and low, stable growth – an environment that favoured long-duration assets such as growth equities and bonds. The inflation shock of 2021-22 disrupted that regime dramatically. Inflation surged, taking the world from disinflationary boom to inflationary boom. Bonds collapsed, commodities briefly took leadership and value took up the running from growth.

Then it was all change again. As inflation moderated during 2023-25, growth stocks surged once more as markets returned to a familiar “Goldilocks” backdrop – resilient growth, falling inflation and eventually lower interest rates.

But could we now be on the verge of another important shift?

At present, markets are displaying characteristics of two different macro regimes simultaneously. On one side, AI-related growth sectors continue to perform extremely well. Investors remain willing to pay high multiples for companies exposed to artificial intelligence, semiconductors, cloud infrastructure and data centres. That behaviour is entirely consistent with a disinflationary boom.

But elsewhere in the markets, a different message is emerging. Commodity-related equities – especially energy – are also performing well. Bonds have stopped behaving as though inflation is fully under control. Long-term yields remain elevated and bond markets have struggled to sustain rallies despite periodic growth scares.

Historically, these leadership groups rarely coexist for long. Growth stocks tend to dominate when inflation is falling, and interest rates are declining. Commodities and energy tend to outperform when nominal growth and inflation are rising.

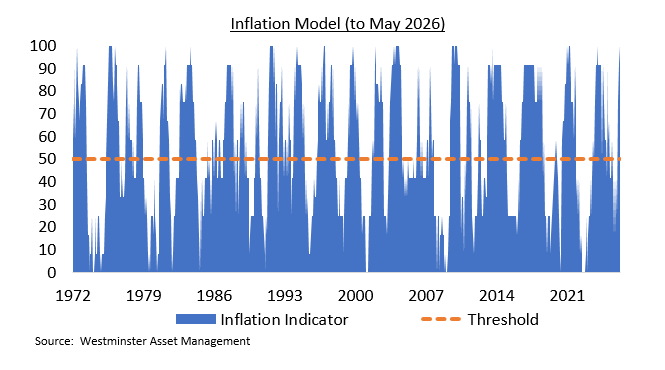

Right now, the inflation evidence is mixed. Inflation has risen and can no longer be described as low. Reflecting pressures emanating from the commodity markets, my inflation model is firmly in accelerating mode. However, trend indicators remain mixed and have yet to confirm a full move into inflationary boom territory.

In short, in keeping with the mixed market picture, we are currently straddling the two inflation quadrants.

From an economic growth perspective, the scare that accompanied the start of the Iran conflict has apparently passed, due largely to the vast amounts of money being invested in the AI space. The Atlanta Fed’s NowCast estimate of nominal economic growth is back above 6%, having briefly dipped to 2%. My own economic growth model is also firmly in accelerating territory. In short, the American economy is experiencing a boom rather than a bust.

If US inflation enters a sustained uptrend and breaches 4%, it would likely herald the start of a very different market regime – one that increasingly favours value stocks, commodities, energy and real assets. Government bonds would likely remain under pressure. Meanwhile, the backdrop would become progressively less friendly for long-duration growth equities, just as speculation surrounding the AI story reaches fever pitch.

The last time we transitioned to an inflationary boom was June 2021. The Nasdaq peaked five months later before experiencing a 37% drawdown in 2022. When the quadrants change, the consequences for markets and investors are usually profound.

Peter Lucas – May 2026