Rethinking Bonds – by Peter Lucas, Westminster Asset Management

“Rethinking bonds”: Westminster Asset Management Investment Strategist Peter Lucas looks at government bonds, and the role they have played in diversified multi-asset portfolios. Peter believes the traditional diversification benefit government bonds offered versus equities is unlikely to hold in the future, with potentially significant implications for portfolio construction going forward.

Government bonds have long been a cornerstone of diversified portfolios, and for good reason. For almost forty years, they delivered equity-like returns with significantly lower volatility. Crucially, they tended to perform well when equities struggled, making them highly effective portfolio insurance.

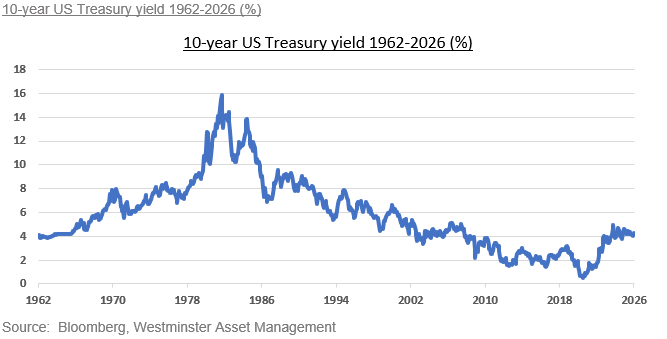

But that period now looks increasingly like an historical anomaly rather than a reliable template. It was shaped by a unique starting point: the exceptionally high inflation and bond yields of the 1970s. From that peak, a multi-decade disinflationary trend drove a powerful re-rating in both bonds and equities.

Viewed over a longer horizon, the picture is less flattering. Bonds have consistently lagged equities in real terms, and their correlation with equities has not always been negative. The diversification benefits investors came to rely on were contingent, not structural.

At a deeper level, there is tension at the heart of the system. Competitive forces within capitalism tend to push costs down over time through innovation, efficiency, and scale. However, modern economies no longer operate under a regime that allows those forces to translate into sustained price stability or deflation. The abandonment of monetary anchors such as the gold standard, the rise of fiat money, and the increasing role of policy in stabilising growth have created a system biased toward positive inflation.

The 1970s marked the turning point. The collapse of Bretton Woods, oil shocks, and wage-price dynamics led to persistently high inflation. The policy response that followed – most notably under Paul Volcker – restored credibility and brought inflation down sharply. From the early 1980s onwards, falling inflation and interest rates created a powerful tailwind for financial assets. This was the golden age of the traditional bond-equity portfolio.

However, bonds can only benefit from such a structural re-rating once. Today, yields are no longer high enough to generate outsized capital gains from disinflation. Instead, bond returns are more likely to reflect underlying economic conditions, as they did historically.

More importantly, the macroeconomic backdrop has shifted again. Government debt levels are much higher, and fiscal policy has become more expansionary. The experience of the 2008 financial crisis reinforced the risks of deflation in a highly leveraged system, leading policymakers to respond more aggressively to downturns. The bias of policy is now asymmetric: deflation is resisted forcefully, while moderate inflation is tolerated.

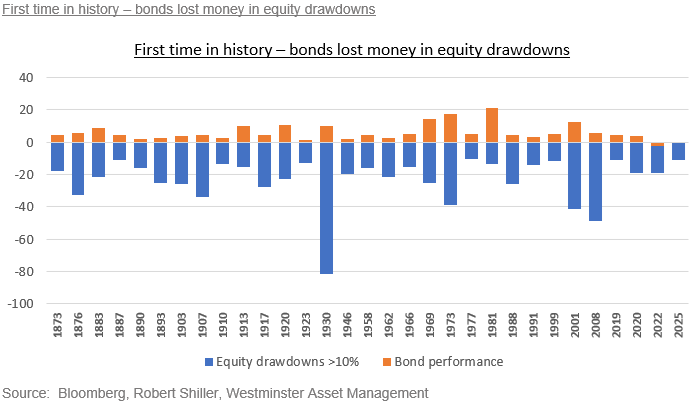

The risks outlined above are not hypothetical. They were visible in 2022, when inflation surged and both equities and government bonds fell sharply at the same time. For the first time in decades, the traditional diversification benefit failed precisely when it was most needed. Balanced portfolios suffered significant drawdowns, particularly in real terms, as rising yields drove losses in bonds while simultaneously compressing equity valuations. While a single year does not define a regime, it served as a clear reminder that bonds are unlikely to provide protection in an inflation-driven shock.

This has important implications for government bonds. Their perceived “risk-free” status rests on two assumptions: that governments will honour their obligations, and that inflation and interest rates will fall during periods of stress. Both assumptions are now less secure. While outright default remains unlikely for countries that issue debt in their own currency, inflation can act as a form of implicit default by eroding the real value of repayments. As a result, government bonds are unlikely to provide the same degree of protection they once did. Volatility is likely to be higher than in the period from 1980 to 2020, and the correlation between bonds and equities may be less reliably negative – particularly in inflation-driven shocks. This raises the risk of larger drawdowns in traditional portfolios, especially in real terms.

Investors may need to rethink the role of defensive assets. Short-duration credit, more flexible or active strategies, and real assets such as commodities may offer more resilient sources of diversification. Within equities, environments characterised by higher and more volatile inflation have historically favoured value-oriented sectors over long-duration growth assets.

Government bonds were not inherently superior diversifiers; they were the beneficiaries of a uniquely favourable macroeconomic backdrop. That backdrop – high starting yields, falling inflation, and ever lower interest rates – will not be repeated. In a world of elevated debt and a structural bias toward inflation, bonds are more likely to behave like cyclical assets than reliable insurance. Portfolios built on the assumptions of the past forty years may discover, at the worst possible moment, that their insurance no longer pays out.

Peter Lucas – March 2026